Instacart S1 Teardown

(MapleBear Inc.) Instacart, the grocery delivery platform that came on its own during the pandemic is gearing up for an IPO, here is everything you need to know about the company.

Editor’s Note: Thank you to 154 new people who decided to subscribe to our newsletter, including execs from Mastercard, Datadog, and Doordash. If you are looking to get your hands on Instacart’s secondary market stock before it goes public, please reach out to us.

Instacart, the grocery delivery platform, filled its S1 for its public debut last week. The company was planning to go public in 2022 but needed to delay its plans due to the worsening conditions of the financial markets due to recession fears.

In the run-up to its IPO, PepsiCo is looking to invest in the company and has agreed to purchase $175 million in stock in a private placement. In all, Instacart has raised nearly $3 billion in total funding since 2012, over a total of 19 rounds, according to data from Crunchbase. In early 2021, the company raised $265 million from Andreessen Horowitz, T. Rowe Price, Sequoia Capital, D1 Capital Partners, and Fidelity Management and Research.

Instacart S1 key takeaways:

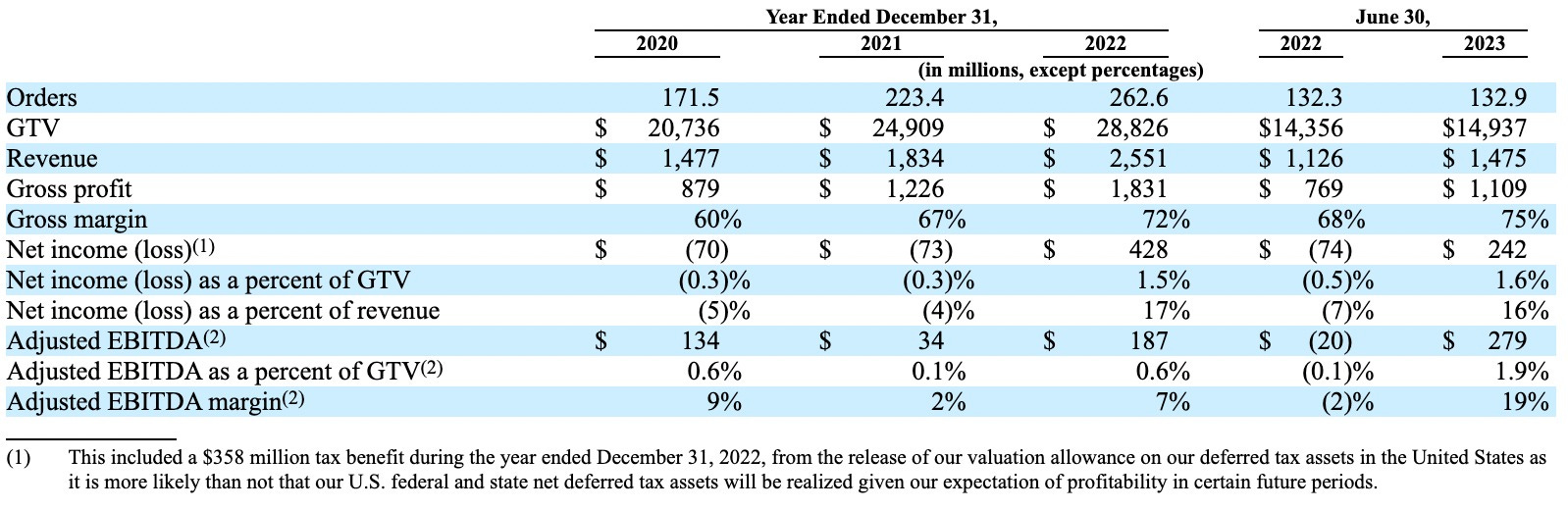

Orders - 262.6M in 2022 (+18%)

GMV - $28.8Bn in 2022 (+16%)

Transaction Revenue - $1.07Bn in H1 2023 (+38%) from H1 2022

Advertising Revenue - $740Mn in 2022 (+29%)

EBITDA (Adjusted) - $279Mn in H1 2023

Net Income (actual) - $27Mn in H1 2023

EBITDA & Adjusted EBITDA

The biggest news that came out of (MapleBear Inc.) Instacart’s S1 is its profitability.

Its adjusted EBITDA - even though it’s not the most robust of profitability metrics - is constantly showing growth from $34M in 2021 to $187M in 2022. In the first half of 2023, its adjusted EBITDA stood at $279M.

Instacart operates in the category where cash burn is massive, and a way to profitability is slim; this is the reason why most analysts were shocked to see these numbers.

Let’s talk about more robust metrics to check on Instacart’s health - GAAP Operating and net income. In the first half of 2022, Instacart’s operating income was (-)$73M, a figure that showed a massive improvement and jumped to (+)269M in the first half of this year. A super quick turnaround, which points towards the agility of the company and its business.

Its net income is a little tricky because of some accounting differences. The company reported (-)$74M as its net income in the first half of 2022, but the company managed to flip that number to (+)$27M in the first of 2023.

Advertising Revenue

During the pandemic, Instacart’s entire focus was on its grocery business, and it showed tremendous growth due to the external tailwind. But during this period, we also found out that the company grew its second revenue stream through advertising to a significant portion.

In 2021, the company reported $572M in revenues from advertising, a massive 31% of its total revenue. The number grew to $740M, but its share in the total revenue decreased to 29%.

The company, in the first half of 2023, reported that it made $406M in revenues from advertising; if all goes well, there is a possibility that by the end of the year, Instacart will hit $1B in advertising revenues. What more can you expect from a secondary business line that is still in the “early stages” of development?

Orders & Cash Flow

Instacart currently generates $1M a day in operating cash flow.

The company generated (+)$277M in 2022, which is surprising when you compare it with their 2021 numbers - the company’s operation burned $204M, a quick turnaround just in time for an IPO.

In the first half of 2022, the company’s operating cash flow was at $99M. The number quickly climbed to $242M in the first half of 2023.

The number of orders is also showing no sign of a slowdown.

In 2022, the number of orders were up by 18% to 262.6M compared to their 2021 numbers. Gross transaction volume also saw an uptick of %16 to $28.8Bn in 2022 compared to their 2021 numbers.

Turning Point

Instacart’s turning point came when Amazon acquired Whole Foods in 2017, which immediately handed 43% of its GMV to its competitor. Their solution was to “arm the rebels” all the other grocers to compete with Amazon. The company decided to work together with Costco and other big retailers and help them deliver to their customers for a 7-8% take rate.

Currently, Instacart works with 1400+ grocers and offers them delivery services through which their customers can easily get groceries delivered to their homes.

To Sum Things Up

A majority of people expected Instacart to dwindle down once the pandemic was over.

That didn’t prove to be the case for the company; its users are not just sticking around; it’s growing. The company has 7.7M active monthly users who order with $317 in monthly spending on the platform.

The company shows massive agility even though its humongous size and the nature of the business. The company, without losing focus on its grocery business, quickly developed a second revenue stream to protect itself from a slowdown in retail.

The company is the market leader when it comes to delivery intermediaries. It also showed hyper-growth and snatched away market share from the traditional grocery platforms.

All-in-all, tremendous numbers, top-tier management, and a fast-growing market make Instacart an exceptional company, especially in the current volatile market.

Please share this newsletter with your friends, family, and colleagues if you feel that it’ll add value to their lives - probably the best compliment we can get :)

| A guest post by

|